Although there are many different credit scores, your main FICO (Fair Isaac Corp.) score is the gold standard that financial institutions use in deciding whether to lend money or issue credit to consumers. Your FICO score isn’t actually a single score. You have one from each of the three credit reporting agencies – Experian, TransUnion and Equifax. Each FICO score is based exclusively on the report from that credit bureau. The score that FICO reports to lenders could be from any one of its 50 different scoring models, but your main score is the middle score from the three credit bureaus, which may have slightly different data. If you have scores of 720, 750 and 770, you have a FICO score of 750. (And you need to take a hard look at your credit reports because those three numbers are considered wildly different.)

Here’s a rundown of what each category means:

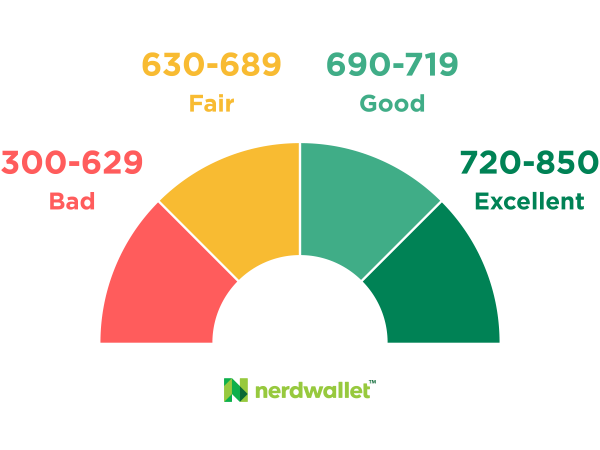

That’s really what you want to know, right? The best-known range of FICO scores is 300-850. Anything above 700 is generally considered to be good. FICO also offers industry-specific FICO scores, such as for credit cards or auto loans, which can range from 250 to 900. There are many FICO versions; FICO 9 is the newest. Mortgage lenders tend to use older FICO score versions.

According to FICO, the higher the score, the lower the risk you pose to a lender. But no score says whether a specific individual will be a “good” or “bad” customer.

FICO undoubtedly has a team of attorneys telling it to drive home the point that it (the company) doesn’t judge somebody’s credit risk. It only reports a score and can provide guidance based on statistical data. A person isn’t a high credit risk per se if they have a 500 FICO score. FICO just reports, based on its statistics, that people with a lower score have defaulted on loans more than those with a higher score. See the difference?

Your credit report can influence your ability to find housing, employment and secure a loan. Knowing your score and understanding your report are the first steps towards your financial health. Our certified financial coaches will guide you through your credit report, answer questions, and give personalized guidance towards improving your score.

Our coaches are certified with the NFCC, so you can be sure your coach will be knowledgeable and professional.

As an NFCC member agency, we are accredited by the Council on Accreditation. This involves regular reviews of our operations to ensure we meet the highest standards for ethics and service delivery.

Before filing for bankruptcy, you are required to complete a pre-filing bankruptcy education session with an EOUST approved credit coach.

Each client’s situation is reviewed carefully by a Coach to ensure we are providing the best possible action plan and advice.

For some, prudent budgeting may not be enough to get out of debt. A Debt Management Plan consolidates all of a client’s monthly credit debt payments into one convenient payment, and brings additional concessions that can lower that monthly payment.

Settlements involve paying less than the amount you owe to make debts go away. If a creditor agrees to settle a debt with you, the resulting notation on your credit report may impact your credit rating.

It may be possible to get debt relief by negotiating with individual creditors, but this leaves you at the mercy of the individual collection agent you speak to and doesn’t address your entire financial situation.